Border Control at the AI Frontier: A Reality Check on Who Owns AI

Anthropic pulled its Fable 5 advanced model three days after launch, under instruction from the US government. Commerce, sovereignty and capability considerations now impinge on our AI adoption...

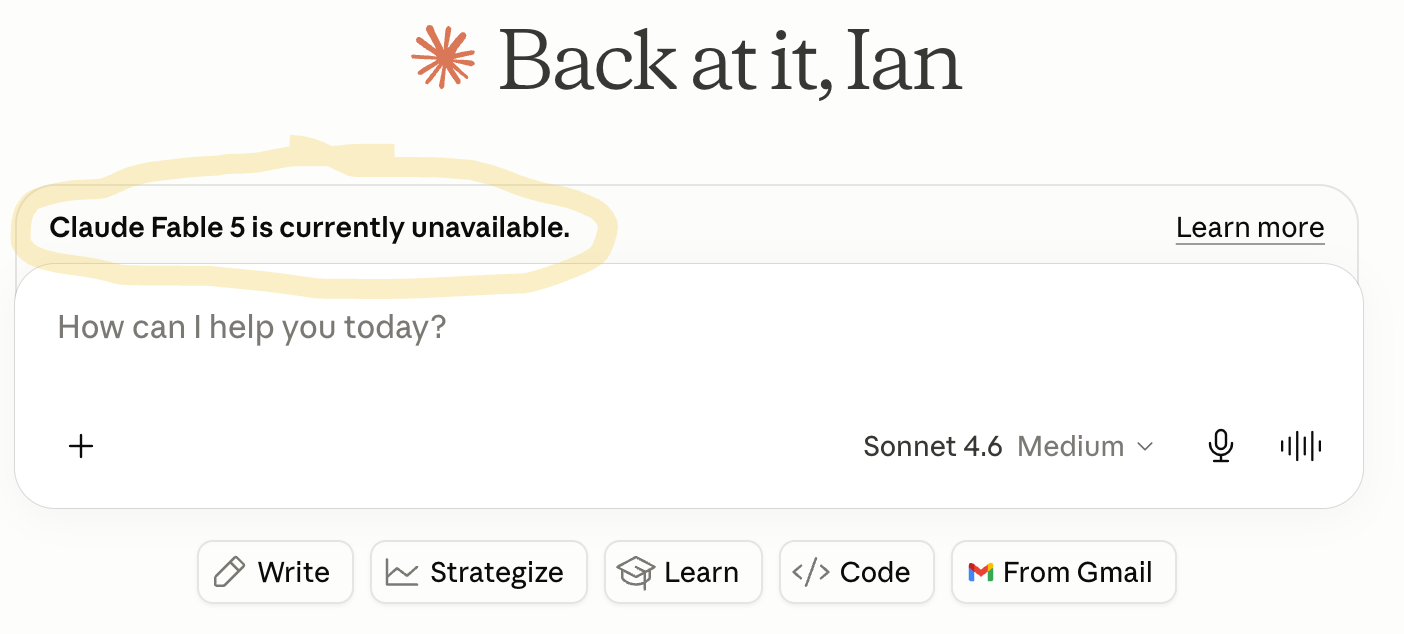

As UK weekend vibecoders will have seen, Claude is displaying that Fable 5 is unavailable. For those like me who cheapskate on Sonnet to preserve tokens and chatting time, this may not seem noteworthy, but the absence of this much-hyped “frontier model” raises questions about AI sovereignty that resonate at the personal, corporate, and country levels.

In short, a US government decision (that the frontier model cannot be used by anyone other than Americans) has brought the issue of state-level control into our AI adoption calculus.

There are some commercial considerations, as well as geopolitical and historical contexts.

In this article

What happened - the Fable 5 / Mythos 5 shut-off in plain language

Ancient history - technology-transfer controls from the Silk Road to semiconductors, plus, of course, the last two years of trade tariffs, provide a background

Cloud/Saas - if you rent, you don’t own (or control)

Three very different readings of the same event - Washington, Beijing, and Europe

Who controls the “on” switch? - nationality as a new parameter in AI access

What the Fable bargain reveals - the EU regulation argument, and the European counter-case

What enterprises (and the rest of us) should actually do - practical considerations, not neo-prepper paranoia

1. What Happened - “Friday evening. Lights out.”

Fable 5 was Anthropic’s “safe” version of the much-hyped Mythos model. It was touted as the next leap in AI, priced accordingly and launched with impressive claims by Anthropic on 9 June.

On 12 June, the US government issued an export-control directive requiring Anthropic to suspend all access to Fable 5 and Mythos 5 for any foreign national, whether inside or outside the US, including Anthropic’s own foreign-national employees. The notification was triggered in part by conversations between Amazon’s CEO and the US Commerce Department as part of ongoing discussions on advanced AI’s capabilities (per the Wall Street Journal 💰and others). Since Amazon is an investor in Anthropic, I’m not sure that this was the intended impact of the conversation, but here we are.

I’m not sure how Anthropic could comply effectively, so they took both models offline globally. Anthropic issued a statement about their compliance that is remarkably restrained (IMO) and does not quite disagree with the government’s reasoning. No point poking the bear in public, I suppose.

There’s no SLA when the US Government issues a decree.

Frankly, the removal of the models doesn’t affect most users, and we will continue to have access to the existing Claude models and services. However, the fact that an AI service can be terminated so abruptly and without notice is a commercial risk to factor into our adoption of and plans for AI.

2. This Is Ancient History - “Glassmakers, gunpowder, and the Nvidia chip ban”

Controlling the flow of powerful technology is as old as powerful technology. It’s not a new instinct; just a new medium.

Some historical examples of limiting foreign access to technology for security, power, and trade advantages…

Murano glass (1271-1295 AD)

The Republic of Venice banned foreign glassworkers from the industry in 12711. Twenty years later, it moved all glass production to the island of Murano, officially a fire precaution, actually an access-control mechanism. Glassblowers gained status (the right to wear swords and for daughters to marry into noble families), but in exchange, they were physically confined. Leaving the island without permission was a capital offence. Some defected anyway and set up competing furnaces in England and the Netherlands. The secrets eventually got out.Gunpowder and the Silk Road

Gunpowder was a Chinese monopoly for roughly six centuries. It reached Europe in the 13th century not as a licensed technology transfer but through trade and contact. The Chinese state attempted to control production and knowledge workers and to prohibit the publication of gunpowder manuals. However, by 1350, English and French armies were using it.Modern export controls: chips, weapons, reactors

Beyond the global trade in commodities, certain goods are deemed too precious to trade, lest the state’s monopoly or advantage be lost. Nuclear technology, advanced semiconductors (the CHIPS Act, Nvidia A100/H100 restrictions on China), weapons platforms.

From GM seeds to chips, software, minerals and arms, the modern state wants to maintain an advantage, even over allies.

3. The Cloud - “You don’t own what you can’t access”

Cloud capabilities (storage, processing, deployment) and SaaS offerings have defined the last decade. This isn’t the place to sing their many praises, but rather I’ll note that:

Even if you own the data in your cloud, it may as well not exist if you can’t access it

SaaS is at the mercy of your provider, access and service levels.

As we’ve seen in wars, national firewalls, electricity brown-outs, withdrawal of payment access (Russia was excluded by SWIFT in 2022), we may cheer some exclusions, and work around others, but the new reality is that we have to plan for the denial of key digital infrastructure and capability.

AI is the newest addition to the contingency planning list.

The nuance is that the exclusion is now characterised by nationality (not national territory).

4. Three Readings - “Washington, Beijing, and the EU”

The perspectives on this will vary by capital (city):

Washington: The US logic is internally consistent even if the execution looks rushed. Frontier models with dual-use cybersecurity capability are, in national-security terms, in the same category as advanced chips and encryption algorithms. The export-control framework exists for exactly this kind of asset. What’s new is the extension from hardware (chips) to software (models), “chips are inputs, models are capabilities”, and the use of emergency verbal directive rather than statutory process. Anthropic accepted the legitimacy of oversight while disputing the process. Their rapid action takes the heat out of a debate with the Executive, and it may, in time, be reversed. However, for Europeans, it’s a reminder that the main AI players are US-based and answer to the US government.

Beijing: Chinese policy has pushed AI self-reliance for years: domestic chips, domestic models, domestic inference infrastructure. DeepSeek’s emergence is viewed as prescience, and their capabilities in AI chips have also been spurred by exclusion. That the directive is couched in nationalist terms will rankle the Chinese; however, they have long prohibited foreign companies from establishing operations in security or technology fields, so the pot and kettle could have a good chat about this.

UK/EU: The UK invested heavily in proximity to US frontier AI as a strategic posture - in cash as well as political capital - through the AI Safety Institute, the Bletchley commitments, and the general position as trusted interlocutor between Washington and Brussels. None of that provided insulation here.

“Ally” is not a category US export-control law recognises at the individual access level. A British national and a Chinese national are both “foreign nationals” in the relevant sense. European enterprise CIOs who treated geopolitical alignment as an implicit guarantee of access continuity need to update that assumption.

France in particular has been clear in seeking an independent (ok, “non-US”) path for its technology: Minitel in the 1980s, Mintel, Pleiades (satellite imaging), Mistral.ai, Ariane (satellites), Rafale (weapons), Galileo (European GPS alternative, led by France). We talk of American Exceptionalism, but France’s exceptionalist streak is rooted in post-War Gaullist views of nuclear independence from the US - the ‘force de frappe’. This is a topic for a future article, but as the reliability of partners and the world order are in doubt, nations must secure their resources. All very 18th century!

5. Who Controls the “On” Switch? -“Not where you are. Who you are.”

The specific novelty is nationality-based access control, not territory, not corporate entity, not contractual relationship. Nationality is individual, non-transferable, and cannot be resolved by VPN, corporate restructuring, or contractual workaround.

This is a world view of “people like us”, “people inside the tent”.

Three concrete implications:

Identity and access management (IAM)

Traditional SaaS IAM works on location, IP, corporate login, and contractual relationship. There is no established infrastructure for managing workforce nationality at the model-access layer. Vendors managed it this time through blanket withdrawal, the only immediately workable option. The principle is now established; will future access models require proof of nationality? Purity of thought and intent? It’s a far cry from username and password! Being cynical, can we even trust software companies to manage this system? After all, these are people who claim not to be able to tackle child abuse, money laundering or extortion, yet are somehow able to charge those users money for services… 🤔Cross-border R&D teams

A mixed-nationality European technical team, British, German, Indian, and Brazilian, using the same enterprise model subscription, has, in principle, different theoretical access rights to the most capable models depending on their passports. Financial services companies have been doing this under anti-money laundering (AML) and ‘know your client’ (KYC) regimes for decades. It is commercially and operationally disruptive, and it raises employment law questions that have not yet been asked, let alone questions about outsourcing, partnering, global team structures… and effectiveness (given the ‘success’ of AML legislation).The “ally” illusion

Equally, the “rule of law” or “customer” illusion.

There’s no court or arbiter that has been able to keep up with the changes in trade, tariffs and access over the last two years. This is a structural reality that needs to be priced into strategic planning.

6. EU: “Regulating or innovating? Why not neither?”

Some commentators decry the lack of a European-grown alternative to the US-led AI revolution: OpenAI, Perplexity, Microsoft, Anthropic, Google, Amazon… Not to mention the AI-weapons economy with Anduriil, Palentir, etc. The claim is that Europe is fiddling (issuing protective legislation) while the continent burns (fails to innovate).

Erik Hedlund wrote a pacey article, berating the EU’s political classes for trading long-term sovereignty for short-term convenience (AI, could also say energy policy). The closeness to the US allowed the continent to walk tall in that shadow, but made us “renters rather than owners”. He has a nice closing point:

“The landlord changed the locks” at 5:21pm Friday. “If your advantage relies entirely on a switch controlled by a foreign power, you do not have a strategy. You have a dependency.”

I don’t entirely agree (although his criticisms have to be considered. Indeed, Ukraine - with its world-leading expertise in drone warfare and adaptive military - also criticises the slow, fragmented pace of Europe’s military response2).

Some thoughts, pending a deeper article:

Europe controls access to a US-sized pool of relatively wealthy consumers (300mn+). Without these, the US companies have a lower addressable market. There’s no evidence that European citizens want to be turned into ‘cyber-surfs’ or neo-peasants for global companies - whether those be Chinese, American (or even other European neighbours). A fair and predictable market is a stable one…

Guardrails and predictability aid commerce (I can’t believe that the US-based tech companies relish the see-saw of legislation and trade, even when they are short-term beneficiaries). Indeed, the word “short-term” is a depressive factor in trade

Europe isn’t an AI-free zone that Hedlund implies (see above on Mistral)

There’s a question as to whether we would benefit from a period of using (and gaining advantage from) AI, rather than the continuous pace of upgrades. A case of avoiding too much progress too quickly.

This last point deserves more space, but for now it’s worth looking at a section in Azeem Azhar’s recent newsletter (“Time to Pause”), referencing calls from the leading AI players to slow model releases. With IPOs on the horizon for all of them, it's time to harvest the economic value of their services, rather than the pell-mell race for feature release and promises of future value.

The key consideration is that Europe, China, and the US view AI capabilities as strategic national tools. This will stimulate protectionist urges (to exploit power and defend against perceived weakness), while stimulating innovation in the secondary or excluded regions, pushing the corporate leaders to consider cartel-like behaviour for mutual benefit. In short, the 2020s resemble the 1920s!

7. So what? - “Practical considerations. Not neo-prepper paranoia.”

The impact is at three levels: our own activities as vibe-coders and AI users; at board level in our businesses; and at a national policy level.

Personal / vibe-coder level

Understand which models you actually depend on for what. What options would you have on personal learning, productivity and workflow if your main AI partner service is removed? The “two is one, and one is none” axiom (from military planning and prepper orthodoxy) is one consideration. Never rely on a single AI.

Consider what data you own, where it’s held and what options there are for Sovereign AI in your work

Know your fallback. Claude Sonnet still works. Gemini still works. GPT still works (even though its own advanced models are as capable as the just-limited Fable 5…). The frontier models are a minority of actual daily use.

If you’re building on frontier-model APIs, note the risk and consider an abstraction layer, and lock in learnings in local data, stores, prompts, workflow and knowledge.

Enterprise / CIO level:

Single-provider dependency on frontier AI is now a documented risk, not a theoretical one. “AI model withdrawal” is a new section in the business continuity planning awayday agenda!

Multi-model routing (an internal AI gateway that can redirect work based on jurisdiction, availability, and cost) is a modest investment, but it’s moved up the priority list

Capability tiering: not every task needs the frontier model. Most retail, operational and creative AI tasks run adequately on smaller, more geographically stable models. Are there opportunities for earlier-generation AI models that your business can own, train and optimise? Value harvesting and independence - a sort of “belay” strategy - can live alongside early adoption

Country / policy level:

Investment in European model capability (Mistral and equivalents) is a genuine hedge, not just an industrial policy gesture.

Open-weight models (Llama, Mistral) running on-premise or in jurisdictionally controlled cloud are not equivalent to frontier models, but they cannot be switched off by a Friday-evening directive.

The governance framework for frontier AI needs to exist. It doesn’t. That gap is being filled by unilateral executive action, which is a worse outcome than a transparent statutory process.

We’ve been in similar situations with multi-cloud, multi-vendor and multi-technology strategies over the last 20 years. In short, at every time of risk and uncertainty, we hedge our bets and focus on resilience.

Closing thoughts

In the past, I’ve written about AI Sovereignty from the perspective of the customer. Now we need to consider Sovereignty from the perspective of the knowledge-working leader, the corporation and the country.

The reality today is that nothing has changed in terms of AI access or capabilities, but the outlook is now riskier. AI is no longer a neutral offering from the US tech giants, but a less predictable puck in a no-holds-barred global game. The tech vendors have an opportunity to ‘innovate at the speed of market exploitation’ (a pause for profitability), while users have to consider their own asymmetrical bargain of sovereignty, access and value.

Has the move by the US Commerce Department impacted your view on effective, commercial AI adoption or your own personal plans? Do let me know your thoughts.

RetailX’s 2026 Leadership Barometer is on the topic of leaders’ attitudes to AI - please take the survey here: https://retailx.net/leadership-barometer02/

atlasobscura.com/articles/venetian-glass-blowing-secrets

https://ecfr.eu/article/combat-lessons-what-europeans-should-learn-from-ukraine/