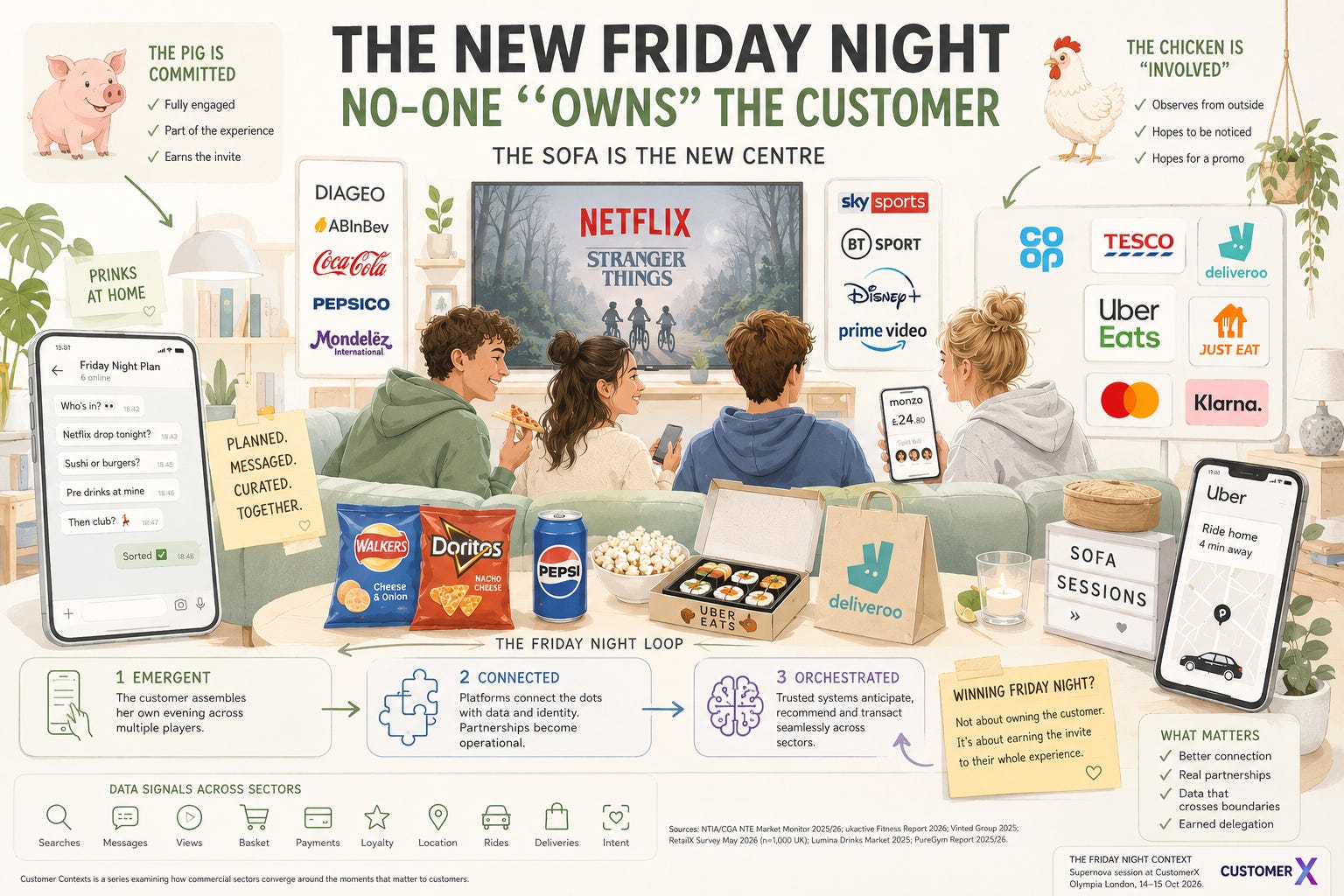

The new Friday night - no-one "owns" the customer

What is the new modality of a Friday night? We consider this emerging Customer Context, why it's more than advertising+, the players, the model and how Boards can position to thrive. Plus a 🐓 and 🐷.

It started with cash

Friday night has been a commercial event for as long as workers have been paid weekly. Google it, kids: a manila envelope, with the workings on the outside, and cash money on the inside. With money in hand and obligations discharged, leisure was briefly possible. Welcome to Friday night.

If we take a clichéd Bert Hardy view, the post-war evening would involve fish and chips, the pub: a defined destination and a social ritual. Each of those businesses was a sector. The pub sold drinks. The chip shop sold food. The cinema, if you went, sold tickets. They did not talk to each other. They did not need to. The customer moved between them, and each business collected its share of the Friday wage, noting the patterns and planning accordingly.

Fast-forward to the 2010s, and an equally broad-brush urban, youthful Friday night would involve a weekend dress (next-day delivery), a group meal (voucher code and group dining promos), cinema tickets (promoted via a tie-up with a mobile phone company)… Then we had the substitutions for the ‘night in’ - streaming movies, home food delivery, and an Uber later to a club after “prinks” or “pres” (pre-drinks) at home to save money.

Optimised sectors

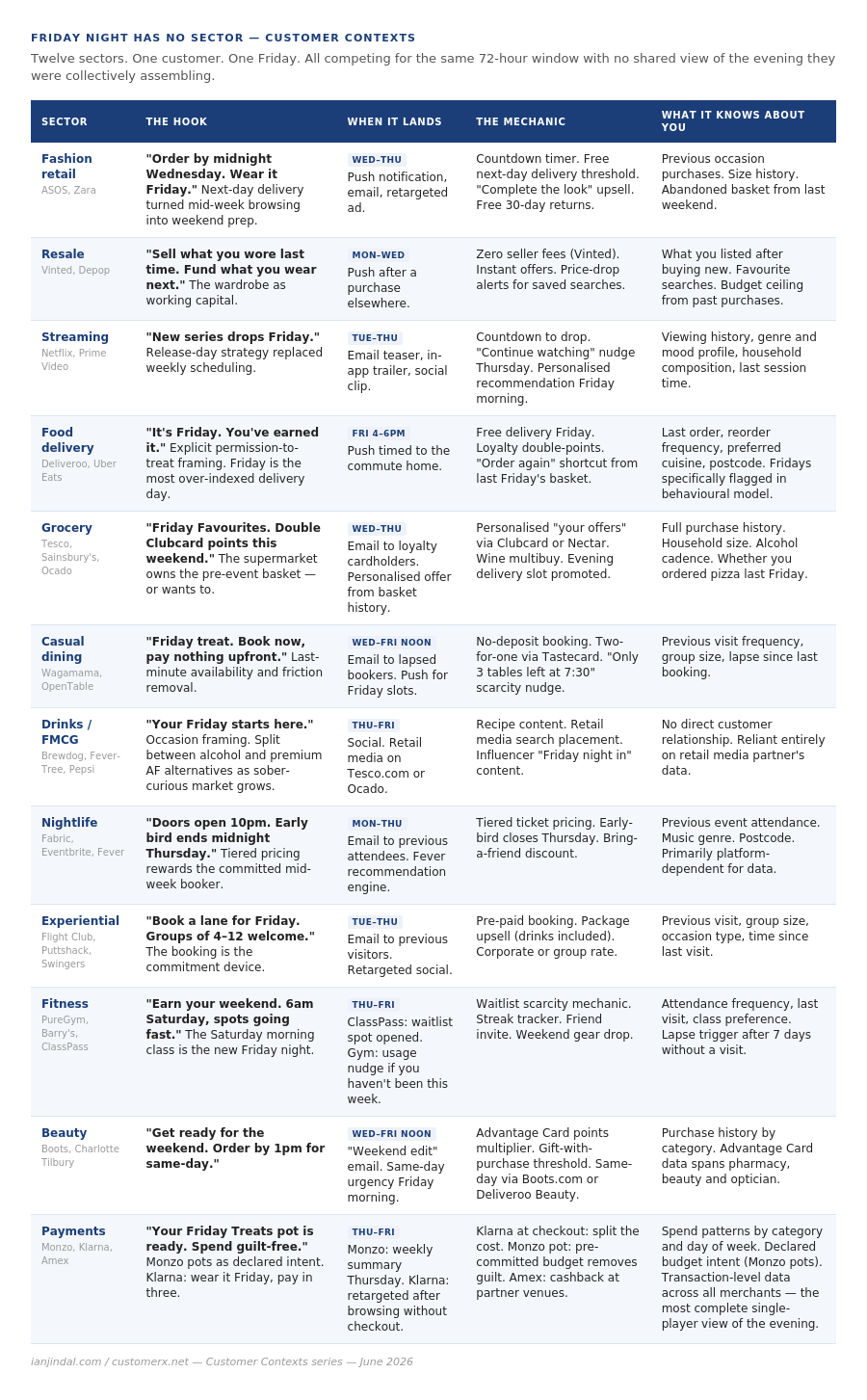

Thanks to data visibility and algorithmic optimisation, each sector ruthlessly and effectively optimised its posture towards the weekly spending opportunity. The table below shows what that looked like in practice: twelve sectors, each with a distinct proposition, all landing in roughly the same 72-hour window, none of them aware of what the others were saying.

Each of these propositions reached the same customer in roughly the same 72-hour window, developed and measured by separate industries with no shared view of the evening they were collectively assembling.

Problem

The problem is not that twelve sectors compete for Friday night. The problem is that each sector sees only its fragment of the customer’s evening. Deliveroo knows you ordered sushi at 7:30 pm. Netflix knows you were in a thriller mood. Tesco knows you bought a bottle of Sancerre on Thursday. Monzo knows the total you spent. None of them knows everything.

The only mechanism any of them had to reach across the boundary - to make themselves present in a moment they did not own - was advertising and co-promotion: a banner, a sponsored placement, a partnership email.

Retail Media’s rise has given more opportunity to be present - piggybacking! - in other moments, but this is not the same as being involved.

General Norman Schwarzkopf is famed for his speech to the troops in the mess hall. He was making a point about the reality of full participation in the conflict and warning against a lack of full engagement. Referencing their breakfast (of ham, eggs, etc.), he commented that:

“The chicken is involved, but the pig is committed”.

The new Friday night marks a shift from Chicken Observer Status to fully engaging with the customer’s entire experience.

Now, we have to admit up front that if two businesses want to collaborate for a promotion, then the tools for this already exist. They still resemble a 4pm-promotional-push where the customer has to create the links herself. The question is whether there’s a broader change. Not a one-off campaign, but an always-on, new modality of behaviour. A new customer context?

The new Friday night: what is actually changing

The shift that is underway is not a better version of the old model. It is the emergence of a different kind of commercial relationship, built on three interlocking changes.

Better connection on the customer’s own surfaces. The phone is not a channel. It is the integration point. The customer who opens Deliveroo from within Netflix, pays with Monzo, earns Tesco Clubcard points on the same transaction, and gets a Gymshark push about Saturday morning’s class - that customer is being served by four sectors simultaneously, on one surface, without switching context. The sectors have not merged. The customer’s surface has. The commercial race is to be present on that surface without requiring the customer to move.

Actual partnerships, not just co-marketing. The signal of genuine structural change is when the integration is operational rather than promotional. Uber Eats carrying Tesco grocery products for 30-minute delivery is not a co-branded ad - it is a shared fulfilment infrastructure. Netflix’s advertising tier moving toward shoppable content is not a sponsorship - it is the attention layer and the transaction layer collapsing into each other. Monzo’s “pots” feature is not a savings product - it is a declared purchase intent signal, pre-segmenting the Friday night customer before she has opened a single app. These are not better ads. They are new commercial arrangements.

Data that crosses sector boundaries. The most consequential change is the least visible. Clean rooms (technical environments in which two companies ask questions of combined datasets without either seeing the other’s raw data) are the infrastructure for sector convergence. Kroger and Disney have clean room arrangements. Tesco and FMCG brands operate within Tesco’s framework. This is not an advertising tool. It is a commercial intelligence tool. The question it answers is not “how do I serve this person a better ad?” but “is this person the same person who behaved in a way that tells me what she will want next Friday?”

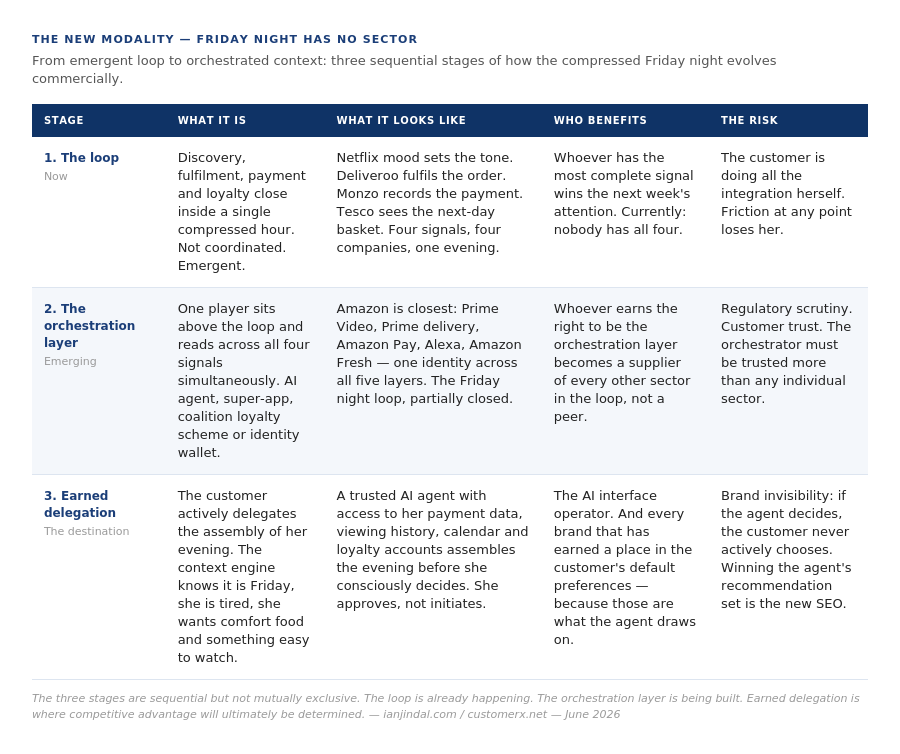

Three stages of the new modality

From emergent to orchestrated: how the compressed context evolves.

The three stages are sequential but not mutually exclusive. The loop is already happening. The orchestration layer is being built. Earned delegation is where competitive advantage will ultimately be determined.

The customer does not care about sectors

She never did. The pub, the chip shop and the cinema did not feel like separate industries to the Friday-night customer of 1965. They felt like Friday night.

The sectors were an organisational convenience - a way for businesses to define their territory, structure their operations and make sense of their competition. The customer’s territory was always the evening itself.

What has changed is that the evening is now technically reconstructible. Every element of it - the outfit, the food, the content, the social occasion, the payment, the loyalty points earned - is gettable, orchestrable and connected.

Not yet seamlessly. Not yet by one player. But directionally, and fast.

Friday night example

Taken from recent sofa sessions with my GenZ offspring. Much planning and chat on WhatsApp, Insta and messaging; Netflix provides a drop or series, with perhaps BT or Sky Sport offering an occasion. Food in the fridge is supplemented by Pepsico adult snacks from the Co-op delivered by Deliveroo, or a meal from Uber Eats, with Diageo drinks in the mix. Payment is via Monzo, using in-app promos and vouchers, splitting the bill and then getting a cab after ‘prinks’ to a club or home with Uber. All moderated via several surfaces - mobile, iPad, laptop, TV screen, Ring doorbell - often as a group.

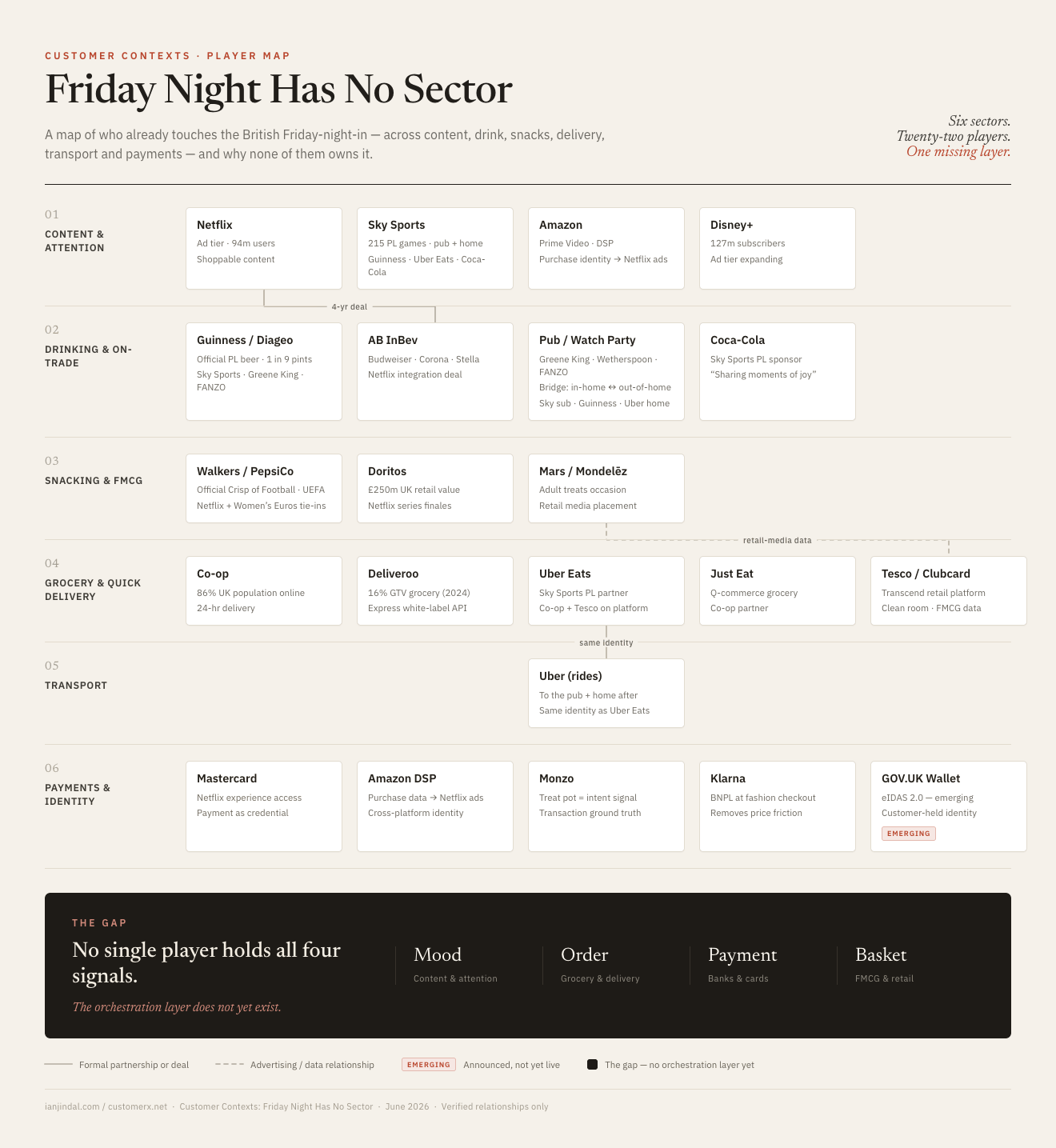

Players

Off the top of my head, we have Netflix, Sky, Amazon, Disney, Diageo, AB Inbev, Coke, Pepsico, Mondelez, Co-op, Deliveroo, Uber, Just Eat, Tesco, Mastercard, Monzo, Klarna… how do these fit together (and where are there gaps)? Here’s Claude Design’s map (based on this article).

“Winning” Friday night

The commercial question is not which sector wins Friday night. It is who earns the right to be present when the customer assembles it. That could be an AI agent. It could be a payments platform that has accumulated sufficient data on declared intent. It could be a coalition loyalty scheme that has signed up enough sectors to see the whole picture. It could be a retailer with a media network, a delivery arm and a financial services offer - if it can persuade the customer to trust it with all three.

The chip shop was not disrupted by a better chip shop.

The Friday night context is not a special case. It is the clearest example of what is happening across every occasion where customer behaviour crosses sector boundaries simultaneously - the gym on Saturday morning, the airport on Monday, the school run, the commute. In each of these contexts, the customer assembles their own experience from multiple commercial players who do not communicate with one another. The question for commercial leaders is not whether this applies to them. It does. The question is which position they occupy in the loop - and whether they are building the capabilities to play a bigger role in it.

Let’s look at some positions and postures.

Positions

Position 1: You hold first-party data

Who: grocery retailers, loyalty scheme operators, payment providers, telcos, banks

You have the most valuable asset in the compressed context - verified behavioural data at the transaction level. The strategic error most organisations in this position are making is treating that data as an advertising product rather than a commercial intelligence asset.

Running a retail media network is not the same as understanding the customer context. Selling inventory to FMCG brands funds the P&L. It does not answer the question of fission. The leaders in this position who will win over the next five years are the ones who use their data to ask a different question: not “which brands want to reach my audience?” but “which partners should I be structurally connected to in order to be present in more of my customers’ occasions?”

The action: Audit your data estate not for advertising value but for context value. What signals do you hold that a partner in a different sector would change their commercial behaviour if they could see? Those are your negotiating assets for structural partnerships, not campaign deals.

The metric to own: Customer occasion share -- not market share within your sector, but share of the customer’s total occasion spend. If your Clubcard data shows someone bought wine on Thursday, but you did not see the Deliveroo order on Friday and the Uber ride home, you are blind to 60% of the commercial event you helped initiate.

Position 2: You do not hold first-party data

Who: FMCG brands, drinks companies, entertainment studios, most consumer brands

You are building on rented land. Every campaign you run through a retail media network, every placement on a streaming platform, every influencer activation - these generate awareness and sometimes conversion, but they do not build a data asset. When the platform changes its algorithm, its pricing, or its partnership model, your commercial model moves with it.

The honest answer for most FMCG and brand leaders is that this is not immediately solvable. You are not going to build a Clubcard. But there are two moves available that most organisations are not making:

First: invest in the occasions rather than the categories. Walkers sponsoring UEFA and embedding in Netflix viewing occasions is not a media buy - it is an attempt to make the brand structurally present in a defined customer context so that the occasion itself triggers the brand, rather than the brand triggering the occasion. That is a different commercial strategy from awareness advertising.

Second: negotiate data access as part of partnership deals, not as an afterthought. When AB InBev signs a deal with Netflix, the question is not just “how many impressions will we get?” but “what signals will we receive about when our brand is present in the viewing context, and can we use that to inform what we put on the shelf at Tesco the following Thursday?” If the answer is no, the partnership is an ad campaign with a longer contract.

The action: Map every partnership and sponsorship you hold against the question: Does this give us a data signal we could not otherwise access? If the answer is consistently no, you are buying awareness. That is fine -- but know that is what you are doing, and price it accordingly.

The metric to own: Occasion penetration -- not just brand penetration. Are you in the basket when the occasion happens, not just in the customer’s awareness?

Position 3: You are a platform or infrastructure player

Who: delivery platforms, payment providers, streaming services, mobility companies, telcos

You are in the most interesting position on the map, and also the most dangerous. You hold the infrastructure of the loop - the logistics, the identity, the payment rail, the attention surface. Every other player in the Friday night context needs you to reach the customer. That makes you structurally powerful. It also makes you a target for regulatory scrutiny, competitive encirclement, and the kind of partnership dependency that can be withdrawn.

The strategic question for platform leaders is: are you building toward orchestration or toward commoditisation? Those are the two endpoints. Orchestration means you become the trusted layer that connects the customer’s contexts - the identity bridge, the preference engine, the interface through which the customer assembles their evening. Commoditisation means you become a logistics or attention provider that any partner can switch to a cheaper alternative.

The difference between those two outcomes is almost entirely determined by one thing: whether the customer trusts you with more than one signal. Deliveroo knows your food order. Uber knows your journey. If Uber knows both - because Uber Eats and Uber rides share an identity - it is closer to orchestration than either one alone.

The companies building toward orchestration are the ones quietly accumulating consent to hold more signals, not just the capability.

The action: Map your current data estate against the Friday night loop. Which signals do you hold? Which adjacent signals would structurally change your commercial model if you could access them with customer consent? Then build the consent architecture, not just the data architecture. The GOV.UK Wallet and eIDAS 2.0 will eventually give customers a portable identity they control. The platform that is trusted enough to be a preferred recipient of that identity will have won the orchestration question.

The metric to own: Signals per customer per occasion -- not transactions per customer. How many of the Friday night loop’s data points do you hold for the same customer in the same evening? That is your orchestration score.

Board questions

In five years, when a customer’s AI agent assembles her Friday evening on her behalf, is our brand, our product, or our platform in the default set it draws from?

That is not a marketing question. It is a commercial strategy question. The agent will draw on loyalty history, transaction data, viewing behaviour, declared preferences, and past occasion patterns. It will not browse. It will not respond to a campaign. It will not be interrupted. It will make decisions based on what the customer has already demonstrated she values - and it will systematically exclude the brands that were not present in those moments.

The customer does not care about sectors. She never did. But she is about to delegate the assembly of her occasions to a system that will care even less. The commercial leaders who understand that are the ones who will be present in the loop. The ones who do not will be advertising to an audience that has already decided.

Friday night has no sector. The companies that win it will be the ones that stopped thinking in sectors first. If the sofa is the new high street, the question is not who owns it, but who the customer invites to join her.

Customer Contexts is a series examining how commercial sectors converge around the moments that matter to customers.

The Friday Night context is the subject of the Supernova session at CustomerX, Olympia London, 14–15 October 2026.

Sources: NTIA/CGA Night Time Economy Market Monitor 2025/26; ukactive Health and Fitness Market Report 2026; Vinted Group 2025 annual results; RetailX Consumer Survey May 2026 (n=1,000 UK); Lumina Intelligence UK Drinks Market 2025; PureGym UK Fitness Report 2025/26.